Whether you’re running a startup built out of your garage or at the helm of an older organization, you need to stay on top of your budget.

If you don’t, you may find that the dreams and ambitions that brought you to your position will remain just barely out of reach.

But how do you go about measuring the financial health of your business?

And, how can you help your business save money in the moments when life gets tough?

Let’s break down the process so that you can get back to making your business dreams become a reality.

Signs of Financial Health

A business’s signs of financial health will vary based on the industry you’re operating in.

In general, though, you can keep an eye out for the following to indicate whether or not you’re on the right track:

#1 Your expenses aren’t growing

As your business grows, you’ll have to diversify the places to which you send your resources.

During that growth phase, you’re going to see your expense costs increase. However, when your business is coming into its own, your expenses should remain fairly consistent.

Expense costs that do not grow over the course of an average financial quarter indicate that your business is looking a-okay, in terms of financial health.

#2 You’re able to put away money

Similarly, the amount of revenue your business is taking in should be on the rise, if your business is in a healthy financial position.

This doesn’t, of course, mean that your revenue should be spiking dramatically, but rather that it should show a gradual upward trend when graphed.

More revenue means more money to expand your business, attend to daily needs, and generally earn back what you may have lost in the company’s initial year of operations.

#3 You have little to no debt

You should also be using your revenue to pay off any debts that you may owe.

A business that is financially healthy will have a low debt rate, to the point where the debt-to-asset ratio lowers significantly.

While you may not have had the chance to clear away your debt entirely, a lower amount of debt partnered with the ability to consistently meet your payments means that your business is serving you well, financially.

#4 Your asset and inventory turnover ratios are high

These activity ratios reflect your business’s ability to maintain and manage assets.

When they’re on the high side, it means that you’re managing your inventory, assessing cost, and operating expenses with care.

#5 You’re bringing in repeat clients

The return of a client after your initial exchange is a good sign for several reasons, the first of which has nothing to do with your finances.

When a client comes back to your business, it means they feel that they can rely on your work. That kind of reliance helps build your industry reputation.

As a result, you’ll be seeing an increased number of clients coming to your business – which, in turn, means more money for you.

Image from Stocksnap.io

Helping Your Business Save

If you’re not seeing signs of your business’s financial health, you may want to take concentrated steps to help save your business money. The different paths you can take include:

A/B test your advertising campaigns

Instead of paying to run multiple variations of an ad campaign at once, be sure to A/B test your work before your debut it. This way, you can save your marketing team money while also capitalizing on your most impactful campaign.

Collaborate with partners or larger businesses

Start-ups or smaller companies might want to consider reaching out to larger businesses to collaborate.

These sorts of collaborations – like, for example, one between a start-up and Amazon through its Amazon Web Services – allow the smaller business partner to access the larger consumer audience, technical know-how, and more. It may be difficult to ask for help, but feel out the larger businesses that may be interested in giving you a hand up. Your business will benefit from your humble approach.

Outsource some of your work

When trying to save money for your business, it may be more responsible for you to outsource some of your resources.

This means working with pre-existing platforms to help pay your employees, manage your Cloud storage, or even host your website.

Work with part-time employees

Many employers are reluctant to hire part-time employees because they’re concerned about their company’s overall time-management.

When you use a time tracking tool like Timeneye, though, you won’t have to worry about anyone falling behind.

Part-time employees not only save you money on employee budgets, but they’ll be able to rotate on your projects courtesy of your company calendar. There’ll be more eyes on your work, as a result, not to mention more money in the bank.

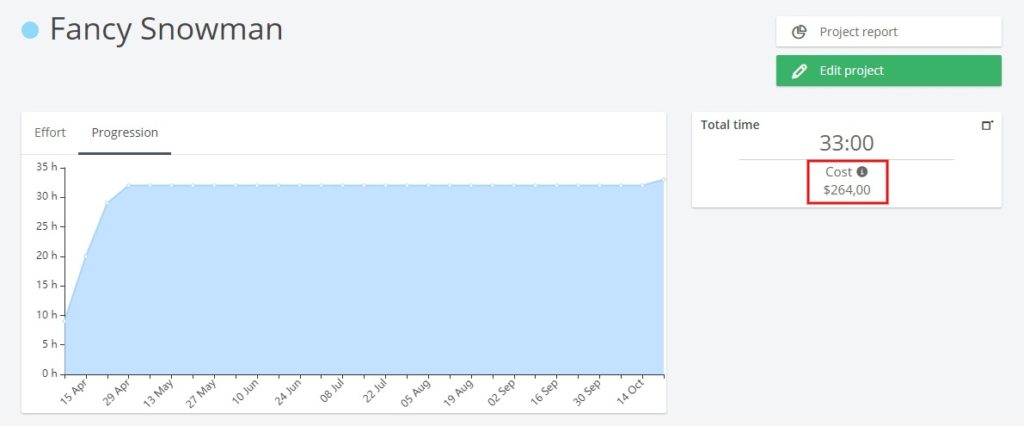

As a plus, Timeneye makes it possible to calculate each employee’s average hourly cost, so you can better decide where your resources should be spent and keep track of assets.

Communicate, communicate, communicate

Above all else, communicate with your clients when you feel that you’re in a financial bind. Some clients may be willing to pre-pay for your services if it means you’ll be able to meet their needs stress-free.

In short, keep an eye on your financial tells to check your business’s health. If you’re not in a good place, there are several different paths you can take to bring your business back up to snuff.